10 Steps to Improve Your Credit Score & Simple, Practical Actions That Work

If you’ve started taking control of your money, the next step is improving something that quietly affects almost every part of your financial life—your credit score.

Whether it’s getting approved for a loan, renting an apartment, or even qualifying for better interest rates, your credit score plays a bigger role than most people realize.

The good news?

You don’t need complicated strategies or financial expertise to improve it. You just need a few consistent, practical habits—the same kind you’re already building.

Let’s walk through it together.

⚠️ A Quick Note Before We Start

This is not financial advice—just practical steps, personal insights, and simple habits that have helped many people improve their credit over time.

Why Your Credit Score Matters - Without Overcomplicating It

Think of your credit score as a trust score.

It tells lenders one simple thing:

👉 “Can this person handle borrowed money responsibly?”

The higher your score, the more trust you build—and that usually means the following:

- Lower interest rates

- Better loan options

- Less financial stress overall

10 Practical Steps to Improve Your Credit Score

1. Pay Your Bills On Time (This Is the Big One)

If you do only one thing—make it this.

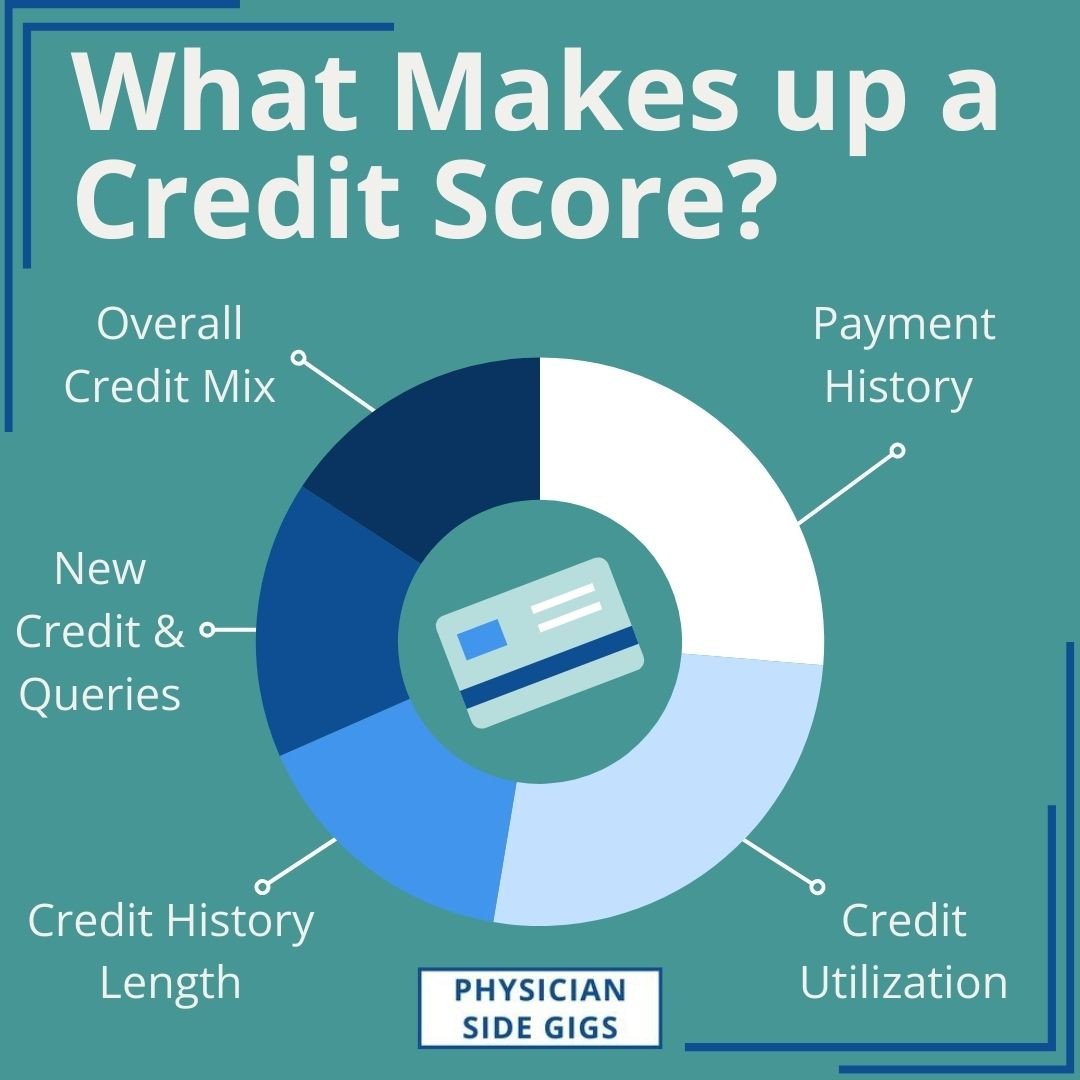

Payment history is the largest factor in your credit score.

Simple way to stay consistent:

- Set up auto-pay for minimum payments

- Use reminders on your phone

- Align bills with your payday

💡 Even one missed payment can hurt your score—but consistency builds it back up over time.

2. Keep Your Credit Card Balances Low

This is called your credit utilization ratio.

👉 Try to use less than 30% of your available credit

👉 Even better: aim for under 10%

Example:

If your limit is $1,000:

- Keep your balance under $300 (ideally under $100)

💡 This shows lenders that you’re not overly reliant on credit.

3. Don’t Close Old Credit Accounts

It might feel like a fresh start, but it can actually hurt your score.

Why?

- It shortens your credit history

- It reduces your available credit

👉 Instead:

Keep old accounts open (even if you rarely use them)

4. Check Your Credit Report Regularly

Mistakes happen more often than people think.

Look for:

- Incorrect balances

- Accounts that aren’t yours

- Late payments you didn’t miss

💡 Fixing errors can give you a quick score boost.

5. Pay Down Debt Strategically

If you’re already working through debt (like we discussed in your previous post), this step fits right in.

Two simple methods:

- Debt Snowball: Pay off smallest debts first (build momentum)

- Debt Avalanche: Pay off the highest interest first (save money)

💡 Both work—choose the one you’ll stick with.

6. Limit New Credit Applications

Every time you apply for credit, it creates a hard inquiry.

Too many in a short time can lower your score.

👉 Be intentional:

- Only apply when necessary

- Avoid multiple applications at once

7. Use Credit—But Don’t Depend on It

No credit activity can be just as unhelpful as too much.

A simple approach:

- Use your card for a small expense (like groceries or gas)

- Pay it off in full each month

💡 This builds a positive history without creating debt.

8. Increase Your Credit Limit (Carefully)

If used wisely, this can instantly improve your utilization ratio.

Example:

- Balance = $200

- Limit increases from $500 → $1,000

- Utilization drops = better score

👉 Just don’t increase spending along with it.

9. Become an Authorized User (Optional Boost)

If someone you trust has good credit, you can be added to their account.

This can:

- Extend your credit history

- Improve your score faster

💡 Make sure they have strong, consistent payment habits.

10. Be Patient and Stay Consistent

This is the part most people don’t want to hear—but it’s the truth:

👉 Credit improvement takes time.

There’s no quick fix—but there is a clear path.

Small, steady actions → real, lasting results.

How This Fits Into Your Bigger Financial Plan

Improving your credit score isn’t separate from money management—it’s part of it.

When you:

- Budget consistently

- Track your spending

- Pay down debt

👉 Your credit naturally improves along the way.

Final Thoughts: Keep It Simple and Sustainable

You don’t need to be perfect.

You don’t need to do everything at once.

You just need to:

- Stay consistent

- Keep things simple

- Focus on progress, not perfection

Because over time, those small habits turn into something powerful:

👉 Financial confidence and control

💡 Want to Take the Next Step?

If you're working toward becoming debt-free and improving your financial habits, start with a simple plan that fits your life—not one that overwhelms you.

What to Read Next

This post pairs perfectly with:

- “15 Budgeting Challenges (And How to Overcome Them)”

- “How to Budget When You’re in Debt”

- “The Debt Snowball Method (Step-by-Step Guide)”

I have the power to overcome my financial challenges

One thought on “10 Steps to Improve Your Credit Score & Simple, Practical Actions That Work”